Reading Ambitiously 4-4-25

Public & Private markets blur, OpenAI flirts with open source at new $300B valuation, SaaS spy flushes phone down toilet, McDermott enterprise sales G.O.A.T., High Agency & Be a ten

Enjoy this week’s Reading Ambitiously as a podcast entirely generated by AI.

The big idea: No Longer Public. No Longer Private.

Is the convergence of public and private markets going to be as big of a deal as the rise of passive investing?

In the 1990s, it was index funds and ETFs that rewrote the rules. Active gave way to passive. Institutions restructured. Flows changed. And over time, most investors barely noticed the shift—until it defined everything.

Now, something similar may be happening again.

Only this time, the lines aren't between active and passive. They’re between public and private. Between liquid and illiquid. Between price discovery and opacity.

Larry Fink, founder and CEO of BlackRock, thinks so. In his latest annual letter, he doesn't hedge: the convergence of public and private markets will be one of the most important structural shifts in capital markets over the coming decades. And not just in the U.S.—globally.

It’s already happening, and yet most market participants are still using a map that splits the world in two.

For decades, the foundation of modern investing has been the 60/40 portfolio—60% stocks, 40% bonds. Simple, liquid, and time-tested. But Larry Fink (and others) are signaling something new: a 50/30/20 model, where 20% of a portfolio goes to private markets. That’s not a minor adjustment—it’s a shift in how portfolios are being constructed at scale. Institutions have been living this reality for years. But if this is the next chapter of capital markets, it’s Main Street—not Wall Street—that will need to catch up. Most retail investors have never had meaningful access to the private side of the barbell. That’s starting to change.

Why it matters:

The old market boundaries—between public and private, active and passive, institutional and retail—are starting to blur. What’s forming instead is a more fluid, continuous system.

Private markets are entering the public wrapper: Privates are no longer reserved for endowments and family offices. They’re flowing into retirement plans, ETFs, and “democratized” vehicles built by firms like Apollo and Blackstone. Larry Fink called it “convergence.” Marc Rowan called it “the new public markets.” They're both right.

Public markets are becoming passive and illiquid: Price discovery is weakening. Indexation (i.e. the rise of index funds) is crowding out discretion. The number of public companies has shrunk by ~50% since the late 1990s. Liquidity still exists, but it's mostly flowing into the same 100 names. That said, some of the best investors are still finding edge — particularly in overlooked small caps and international markets. And even within ETFs, active strategies just passed $1 trillion in assets for the first time.

Active management hasn’t disappeared—it’s just moved upstream: It’s private equity, private credit, structured solutions. These managers are underwriting complexity, building companies, and shaping outcomes in ways public markets no longer reward. But active management is also alive in the public markets—especially among asset managers who are willing to be contrarian, concentrated, and patient or a close friend of mine says “the capacity to suffer”.

The toolkit is blending: Public companies are adopting private market behaviors—direct listings, dual-class shares, founder majority ownership, limited quarterly guidance. Private companies are adopting public discipline—board governance, KPIs, liquidity programs. The operating models are converging too.

Governance is drifting: With passive managers holding growing stakes in public companies but often abstaining from active stewardship, who’s minding the shop? At the same time, private governance is becoming more standardized—but not necessarily more transparent.

What this means:

This convergence isn’t theoretical—it’s changing how capital flows, how companies grow, and how returns are generated.

For startup founders: The IPO is no longer the finish line. It’s one of many options. Companies can now raise billions, run tender offers, or stay private indefinitely without sacrificing growth or employee liquidity. But the tradeoffs are real—control, visibility, governance, and the cost of capital all show up differently depending on the path.

For main street investors: If 20% of the future portfolio lives in private markets, access becomes the battleground. Historically, retail investors have been shut out of the most compelling private opportunities. That’s beginning to change—with structured vehicles, interval funds, and tokenized infrastructure—but the risk is that performance bifurcates between those who get exposure and those who don’t.

For asset managers: There’s never been a better time to double down on a differentiated edge. As passive strategies become more pervasive, the market is hungry for managers with conviction, clarity, and real insight. But it’s not just about security selection anymore—technology, structural creativity, distribution strategy, and access models are becoming just as important. The firms that combine sharp investment thinking with modern infrastructure will be the ones that break out.

For operators: You’re playing on a hybrid field. Your board might include a sovereign wealth fund, a private equity sponsor, and a public crossover fund—each with different expectations. Your valuation might be shaped by private comp benchmarks and public multiples. You’re not “private” or “public.” You’re navigating both systems at once.

The bottom line:

We’re entering an era of continuous markets—where the real edge belongs to those who can move across categories, not stay confined by them.

The best firms won’t be public or private. They’ll operate across both. The best allocators won’t be active or passive. They’ll understand how to blend. And the best asset managers won’t be defined by size. They’ll be defined by sharp perspective, smart structure, and trusted access.

The convergence of public and private markets isn’t a threat. It’s a design challenge. A strategic opening. An invitation to rethink what it means to build, invest, and compound in a market that’s no longer binary.

“The idea that public and private are two different worlds—that idea is dead.” —Marc Rowan, Apollo CEO

Best of the rest:

🚀 OpenAI Valued at $300 Billion as Sam Altman Teases Open-Weight Model - OpenAI continues its explosive rise—adding one million users per hour—and hints at releasing its first open-weight model in years. - Business Insider

🔄 Scarcity and Abundance in 2025 - Alex Danco reflects on how the forces of scarcity and abundance are shaping tech, capital, and attention in 2025. - Alex Danco

🧪 Favorite Products/AI – Q2 2025 Survey Results - Kevin Rose shares survey insights on the most-loved AI tools and products in this rapidly evolving landscape. - Kevin Rose

🛠️ A Deep Dive Into MCP and the Future of AI Tooling - a16z explores Model-Context-Protocol (MCP) as a framework for understanding the next generation of AI tools and infrastructure. - a16z

Charts that caught my eye:

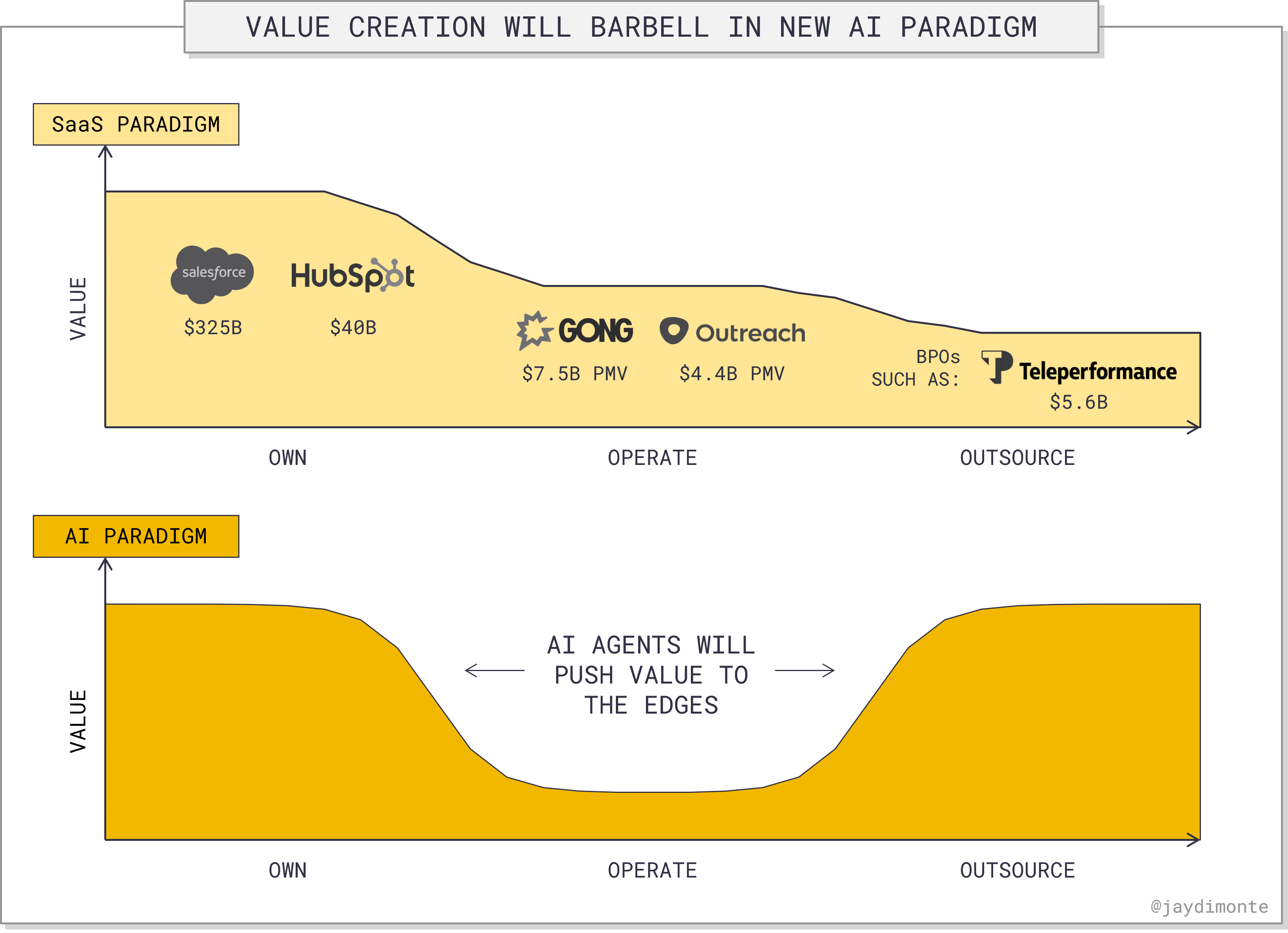

AI Raises a Big Question, but Legacy Industries Have Already Answered It (Day by Jay)

→ Why does it matter? Jackie DiMonte lays out a compelling framework: software companies—like their legacy industry counterparts—tend to create the most enterprise value at the extremes. The “own” model (platforms like Salesforce or Workday) gives customers total control over core workflows. The “outsource” model (AI-enabled service providers) solves undifferentiated problems entirely. Both are durable, scalable, and defensible. The danger zone? The operate middle—tools that sit alongside a system of record but don’t own it.

→ Why does it matter? You’d expect a firm like ThomaBravo to say every company needs to become an intelligent software company—but they might be right. According to this chart, software spend is expected to double from 2% of GDP in 2020 to 4% by 2030. The driver? AI.

Tweets that stopped my scroll:

→ Why does it matter? The Deel vs. Rippling corporate espionage case reads more like a Netflix script than a startup dispute. A former Rippling employee allegedly flushed his phone down the toilet and fled to Europe—only to be offered relocation to Dubai by Deel’s legal team, according to court documents.

Worth a watch or listen at 1x:

→ Why does it matter? Aaron Levie, CEO of Box, lays out a sharp mental model: SaaS was about workflows—AI is about outcomes. In the cloud era, software helped users complete tasks; in the AI era, it will complete the tasks itself. This marks a shift from assistive tools to autonomous agents, with software evolving from UI-centric to results-centric. As Levie puts it: “In SaaS, we sold software. In AI, we’re going to sell intelligence.” That change rewires everything—from how products are built to what creates defensibility.

→ Why does it matter? Bill McDermott didn’t just sell copiers in a two-block patch of New York—he built a mindset. If you work in anything to do with sales, this video is a masterclass. Bill breaks down how to win trust, outwork everyone, and turn small wins into a billion-dollar runway. His story reminds us that the best salespeople don’t sell—they solve. And they never stop showing up.

Quotes & eyewash:

→ Why does it matter? High agency means finding a way to get what you want, without waiting for conditions to be perfect or blaming the circumstances. George Mack spent seven months writing the essay he wished he had as a young adult—a guide to the value found at the intersection of clear thinking, disagreeability, and a bias toward action: high agency.

→ Why does it matter? Steve Schwarzman defines eights as people who can follow marching orders, nines as those who can execute and strategize, and tens as those who can sense problems, design solutions, explore new directions—and make it rain. But here’s the nuance: tens don’t earn that distinction by dazzling with complexity. They earn it by making problems go away. Elegantly. Quietly. Permanently.

The mission:

The Wall Street Journal once used ‘Read Ambitiously’ as a slogan, but it became a challenge I took to heart. If that old slogan still speaks to you, this weekly curated newsletter is for you. Every week, I will summarize the most important and impactful headlines across technology, finance, AI and enterprise SaaS. Together, we can read with an intent to grow, always be learning, and refine our lens to spot the best opportunities. As Jamie Dimon says, “Great leaders are readers.”