Reading Ambitiously 7-25-25

Target date funds add private credit, BlackRock says bring a burner, Oracle's $30B whale is OpenAI, WarrenBuffettGPT, Stripe on API design, GameStop, Acquired interviews Jamie Dimon

This week’s Reading Ambitiously read to you by me and now available on Spotify!

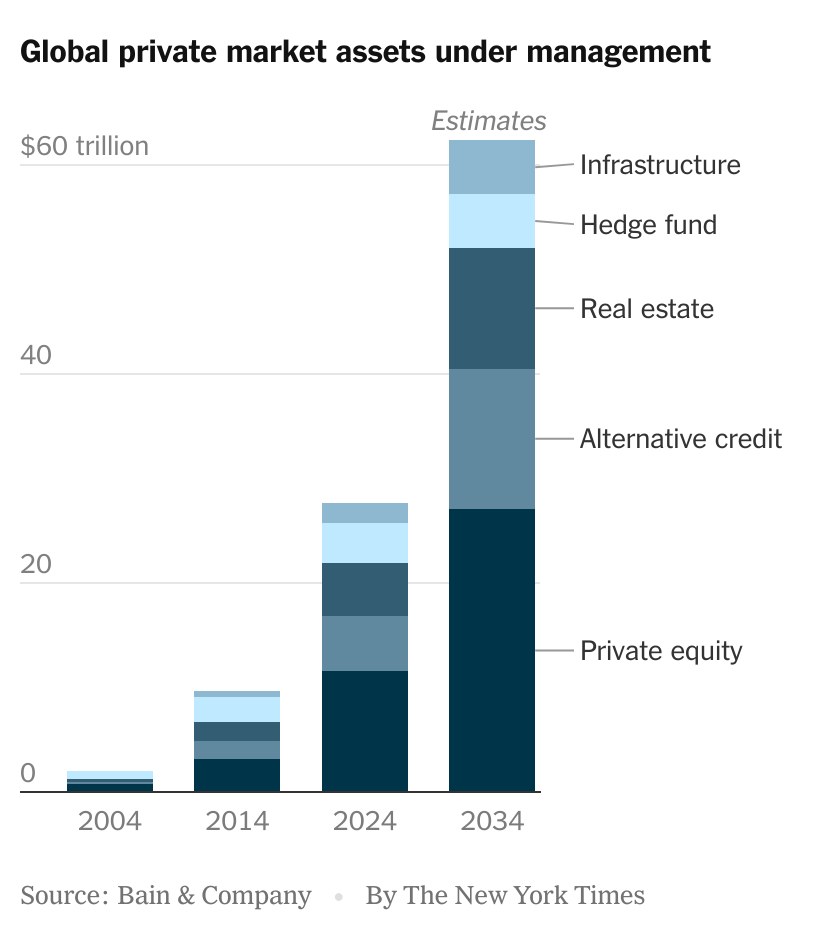

The big idea: Private markets pulled me in. Should they pull in your 401(k) too?

Target Date

I remember it like it was yesterday. My first job at IBM. The standard-issue ThinkPad, setting up LotusNotes (yes, LotusNotes), and onboarding to all the corporate systems. We’ve all experienced it.

One of those systems: Fidelity NetBenefits, where for the first time, I opened a 401(k). After the infamous five questions about my age, objectives, and whether I’d sell in a market downturn, Fidelity recommended the target-date fund. It was 90 percent stocks, 10 percent bonds. Aggressive by design. Over time, it would glide to 60 percent stocks and 40 percent bonds.

That was the standard approach. Set it, forget it, let time and compounding do the work.

Not anymore. Soon, Fidelity and others may be recommending a different asset allocation. Something closer to 50/30/20: 50 percent in public stocks, 30 percent in bonds, and 20 percent in private investments.

That last piece is new. Private investments could include credit, buyouts, even ownership in fast-growing private companies.

Maybe you can’t pick that exact portfolio today, but the question is no longer if. It’s when. And more importantly: how are investors protected when it arrives?

Regulatory Tailwinds

Washington wants to open the retirement system to private markets.

The SEC is studying ways to loosen accredited investor rules. The Department of Labor is revisiting what a 401(k) can include.

Everything is trending toward making the case to open the doors. Asset managers are lining up on the other side.

New funds are launching that blend public and private assets, with varying degrees of liquidity, called interval funds. KKR and Capital Group launched one such fund that mixes public bonds and private credit. It’s positioned as 401(k)-friendly and allows quarterly redemptions. Apollo and State Street rolled out a similar public-private ETF that offers a daily price, backed by Apollo guarantees. Even a tech-forward hedge fund and venture capital leader, Coatue, recently launched an interval fund focused on technology growth.

The product shelf is filling up quickly. And the message is clear: private investments aren’t just for institutions or ultra-high-net-worth individuals anymore. They’re for Main Street.

Main Street Wants a Bite of the Apple

And they should be given one, because the growth in private markets is hard to ignore.

Private assets have also in some cases outperformed traditional asset classes over the past decade. Strong performance and diversification is exactly what retirement savers want.

The advantage isn’t just in the numbers. Megatrends like staying private longer mean that a growing share of value creation now happens well before an IPO.

Platforms like Forge and Robinhood are working to make private markets feel more accessible. Forge now offers shares in companies like SpaceX, Stripe, and OpenAI, with minimums as low as $5,000. Robinhood is experimenting with tokenized shares of private companies in Europe, a move it calls “the next frontier to democratizing investing.” The tools and interest are growing fast.

If these investments offer better returns and better diversification, why should they be reserved for institutions and ultra-wealthy individuals?

There’s a lot of upside here. But that’s only half the story.

Market Cycles

It’s a tricky time to start opening the floodgates.

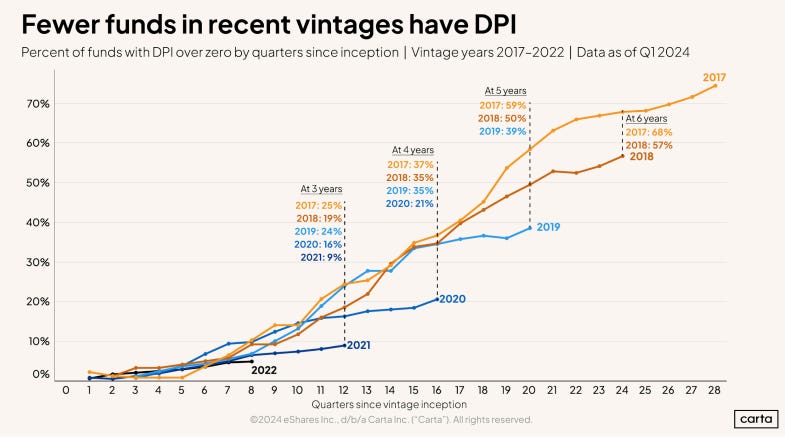

Private equity isn’t exactly having a banner year. Distributions are down. A lot of limited partners haven’t seen meaningful liquidity in a while. Some funds are rolling assets into continuation vehicles just to buy time. DPI is falling. DPI, or distributions to paid-in capital, measures how much cash investors have actually received back relative to what they put in. Recent vintages are lagging badly.

At the same time, interest rates are no longer near zero. That feels like the bigger issue. For decades, private equity thrived in a world of cheap money. It was easier to use leverage, which drove high valuations. Returns looked great.

Howard Marks called this a sea change in his 2022 memo:

“The environment in which we operate is changing in profound ways… the ingredients that made the last 40 years so fruitful may not be present in the years ahead.”

So now we’re going to open private markets to Main Street?

Is this about expanding access or needing a new buyer?

It feels like we’re in the later stages of the cycle, right as we’re about to let retail investors in. And even the insiders are starting to question the model.

"We need to be careful of what we wish for," a longtime private equity exec recently told Axios.

The Case For and Against

There’s a strong case to be made for opening private investments to retirement savers.

Retirement capital is long-dated by nature. These investors have time and many decades ahead. That’s exactly the kind of capital private markets thrive on.

Private assets behave differently than public ones. That diversification can smooth volatility over time.

As companies stay private longer, value creation happens earlier. If the public can’t get in, most of the upside is already spoken for. Opening things up would make for a more inclusive market.

But the other side of this debate is just as real.

Private investments are harder to value. Most are marked quarterly at best, not daily. That can hide risk.

Fees and disclosures aren’t as transparent as in public markets.

And most importantly, liquidity is not guaranteed. In a downturn, it can vanish. Investors who think they can redeem may learn otherwise. When liquidity dries up, it can get ugly.

“Investors in these funds, mostly individuals who paid as little as $2,500, appear worried that their funds might also tighten the withdrawal spigot, forcing them to wait indefinitely in line if they want to cash out.”

Then there’s the timing issue. Late-cycle conditions and the possibility of higher-for-longer rates could put pressure on future returns. The risk isn’t just underperformance. It’s the perception that these investments are safer than they really are.

Why It Matters

This shift is coming. Maybe not all at once, but steadily. Momentum is building.

These aren’t just new products. They represent a structural change in where trillions of dollars in retirement capital are allowed to invest and what risks that capital is allowed to take.

No doubt, the opportunity in private markets is real. Those trends have taken me personally from IBM Big Blue (chip) to Ridgeline, an entirely privately funded venture. The private markets can offer upside, diversification, and access.

But investors deserve to understand what they’re getting into. These assets are illiquid. They’re not priced daily. They have lower standards for disclosure and higher complexity in fees. You can’t sell them like you can IBM.

There’s a lot to figure out. The 20 percent allocation feels like it’s coming.

The question is whether we’ll build the systems, protections, and expectations to handle it.

What’s coming isn’t just a new menu option in your 401(k). It’s a shift in who gets to own the future and who carries the risk when markets turn. That’s the part we can’t afford to get wrong.

Best of the rest:

🔥 The Founder Who Can’t Miss — Ramtin Naimi turned a hot hand into a hedge fund, stumbled early, and is now back on top, rewriting the rules of growth investing before his 35th birthday. — Colossus

🛡️ BlackRock locks down China travel — The world’s largest asset manager is asking staff to buy a “burner phone” before traveling in China, citing security risks amid rising geopolitical tensions and recent travel detentions. – Bloomberg

🤖 GPT-5 Lands in August — OpenAI is set to release its next flagship model next month, but first it's debuting a new open-source model—signaling a more layered strategy for balancing openness, capability, and control. — The Verge

🚀 Inside the Machine: Life at OpenAI — A candid, richly detailed reflection from a former engineer who helped launch Codex offers a rare window into OpenAI’s chaotic ambition, bottoms-up culture, and breakneck pace—highlighting what it really feels like to build the future from inside the eye of the AGI storm. — Calvin French-Owen

🧠 Very Bad Advice — Morgan Housel’s latest is a masterclass in inversion: a sharp, memorable list of what not to do if you want to live wisely and well. – Collaborative Fund

🧱 Point Solutions Can Become Platforms — Clouded Judgement reflects on how giants like Datadog started as niche tools, outmaneuvered incumbents, and became dominant platforms—suggesting today’s “wrappers” could be tomorrow’s winners if they execute with speed and focus. — Clouded Judgement

Charts that caught my eye:

→ Why does it matter? For a long time, headcount was a proxy for influence. Running a big team signaled importance. But in this new wave of AI-native companies, the opposite is often true. The most impressive operators aren’t managing more - they’re doing more with less. This is such a flex that somebody created a leaderboard to track this!

→ Why does it matter? Gem is the leading platform for automating correspondence between talent teams and candidates. They analyzed data from 4M+ outreach campaigns to figure out the best way to write an email—and the right time to send it. What’s striking is how transferable these insights are. This isn’t just for recruiters. These tricks apply to any important email.

→ Why does it matter? Nvidia’s $4 trillion valuation now tops Canada’s entire GDP. The chart puts that into sharp relief—Nvidia alone is worth more than Meta and Alphabet combined, or Amazon, Walmart, and Costco together. Investors aren’t just excited about AI—they’re treating it as the next great industrial revolution, and Nvidia as its core supplier. If the automation economy really will be measured in tens of trillions, this might not be irrational exuberance. It might be early.

→ Why does it matter? Wow. Meta didn’t just build a superintelligence team—they assembled a $10 billion braintrust. H/t to Deedy for surfacing the details: half the team is Chinese, three-quarters have PhDs, and most came straight from OpenAI, DeepMind, or Scale. A lot of these people built the frontier. Zuckerberg reportedly considered offering OpenAI’s Chief of Research a $1B comp package this week. What does he know that we don’t?

Tweets that stopped my scroll:

→ Why does it matter? Aaron Levie just put a spotlight on the quiet infrastructure layer of the agentic era. Everyone’s chasing AI agents, but when you have 100x more agents than humans, the real power shifts to the systems of record—where data lives, where workflows get logged, and where business logic is enforced. Agents need context, history, and structure to stay useful. That’s why deep integration isn’t a feature—it’s the foundation. This was exactly the topic of last week's Reading Ambitiously 7-18-25.

→ Why does it matter? APIs aren’t just technical choices—they're strategic ones. Patrick Collison’s reflection echoes Conway’s Law: organizations design systems that mirror their own communication structure. That means your API surface area quietly reflects your org chart, your product bets, and your customer assumptions. If you want to scale elegantly, start by designing data models that match the business you’re trying to become.

→ Why does it matter? Hit the link and you’ll find a Github repo with this exact prompt to try out yourself!

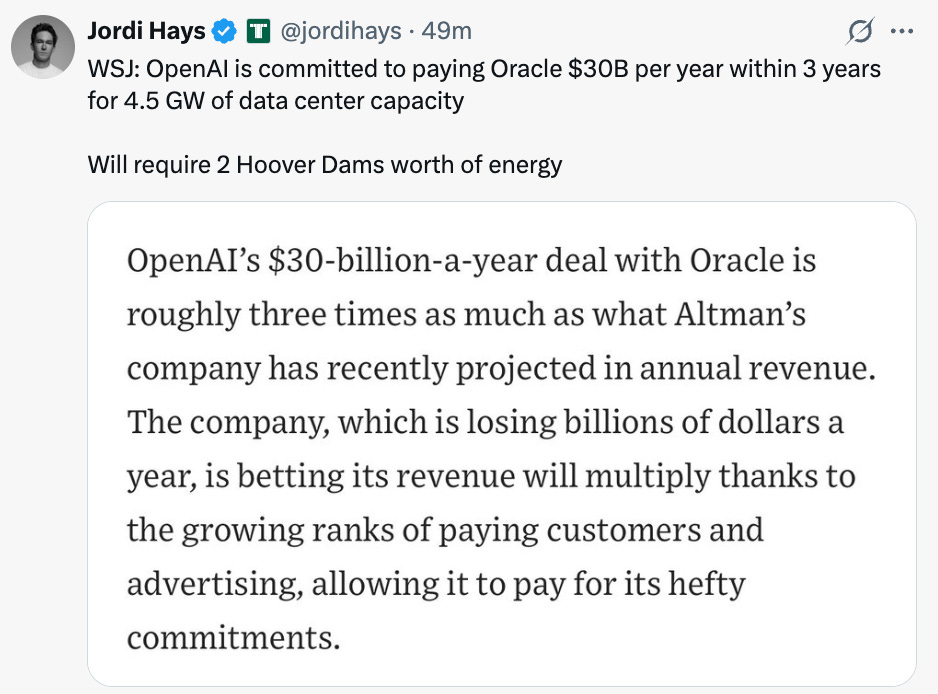

→ Why does it matter? The mystery $30B Oracle deal we reported a few weeks ago? You guessed it, OpenAI. 3x their current annual revenues.

Worth a watch or listen at 1x:

→ Why does it matter? The Acquired crew tells Jamie Dimon’s story with clarity and depth. What stands out most is his move to Bank One—buying stock, betting on himself, and leaving no room for retreat. After getting pushed out of Citigroup, where he was expected to become CEO, he started over with a struggling regional bank. That decision laid the groundwork for JPMorgan Chase to become the most systemically important financial institution in the world. No shortcuts, no safety net. Just execution over time.

→ Why does it matter? Dan Sundheim was one of the institutional heavyweights caught flat-footed during the GameStop frenzy. Short the stock, long the logic, and suddenly underwater. In this interview, he opens up about what it felt like to be in the blast zone and how the experience reshaped his thinking. For a firm like D1, which blends public and private investing, the lesson wasn’t just about risk. It was about humility, velocity, and rebuilding trust. Three years later, Sundheim is still standing and maybe even stronger.

Quotes & eyewash:

→ Why does it matter? A photographer captured the exact moment this mouse was picked up by a bird of prey. The look on the mouses face is priceless.

The mission:

The Wall Street Journal once used ‘Read Ambitiously’ as a slogan, but it became a challenge I took to heart. We aspire to give you a point of view in a noisy, ever-changing world. To unpack the big ideas that sharpen your edge and show why they matter. To fit ambition-sized insight into your busy life. And to channel the zeitgeist into the stories, signals, and substance that fuel your next move as leaders. Together, we can read with an intent to grow, always be learning, and refine our lens to spot the best opportunities. As Jamie Dimon says, “Great leaders are readers.”