Reading Ambitiously 10-17-25

AI Froth, Paradox of Skill, Techno Optimism, SaaS Multiples, JPMs $1.5T plan, AI Slop, Happiness, Thrive Capital, Robots, SFDC installs ChatGPT, Sorkin's 1929

Enjoy this week’s Big Idea read by me:

The big idea: It’s getting frothy out there

On Friday, I caught up with one of our ambitious readers, a well-respected venture capitalist, who ended the call after a long pause: “It’s getting pretty frothy out there.”

No doubt it is.

“In the short term, the stock market is a voting machine; in the long term, it’s a weighing machine.” - Benjamin Graham

The line is sometimes misattributed to Jeff Bezos, who has frequently used it to describe his strategy for building Amazon “heavier” and “heavier”. What he meant by heavy wasn’t size, it was substance. The fundamentals and quality of the Amazon business itself. He once explained it this way:

“The stock is not the company, and the company is not the stock.”

When the dotcom bubble burst, Amazon’s share price fell from $113 to $6. Yet inside the company, Bezos observed that everything was improving. Customers were growing, unit economics were strengthening, and revenues were accelerating. Although the stock took a wrong turn, the business was actually getting stronger.

From those ashes, Amazon emerged as the second-largest Fortune 500 company, trailing only Walmart. Last year, it reported $638 billion in revenue. That’s what heavier looks like. In a rare interview two weeks ago, Bezos said:

“We’re in an AI bubble.” Then he added, “The benefits will be gigantic.”

It’s the kind of paradox he’s always lived comfortably with. F. Scott Fitzgerald once wrote:

“The test of a first-rate intelligence is the ability to hold two opposed ideas in the mind at the same time and still retain the ability to function.”

The same holds here. AI may be the most significant technological shift in a generation, and yet markets may be racing too far ahead of the fundamentals.

It’s getting frothy, and at this stage in the cycle, the deals are getting more creative. The voting machine might reward that creativity in the short term, but in the long run, it will ask a harder question: Are you getting heavier?

The Dollar Merry-Go-Round

In the late 1990s, at the height of the dot-com boom, Web 1.0 companies began experimenting with innovative strategies to drive growth. The tactics varied, but the pattern was the same. They discovered they could trade services with one another, record both sides as revenue, and drive growth without any new money entering the system. Revenue grew exponentially, cash flow did not, and when the bubble burst, much of that growth vanished.

AOL, Yahoo, and Excite traded ad space back and forth, each recording the barter as revenue.

Webvan and HomeGrocer swapped logistics services, booking income on both sides of the ledger.

Global Crossing and Qwest sold each other excess fiber capacity with so-called indefeasible rights of use, inflating their top lines without generating new demand.

The creativity was extraordinary. Mostly legal, yet often, in the grey area of accounting practices. And the results were temporary.

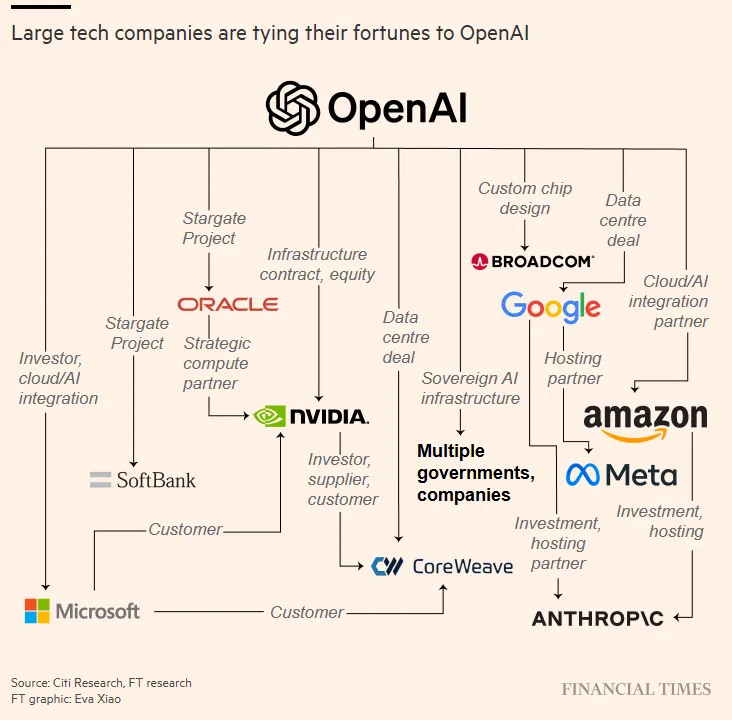

A similar version of this appears to be happening today, only this time, it’s not ad inventory or bandwidth - it’s compute.

Across the AI economy, dollars go from Company A to Company B back to Company A. Nvidia invests in OpenAI. OpenAI spends those funds on Oracle’s cloud. Oracle uses that demand to justify new data centers that require more Nvidia chips. Each participant recognizes growth, but the same capital circulates through the system.

You can see it in the headlines:

Microsoft invests in OpenAI, which in turn becomes one of Azure’s largest customers.

Nvidia sells GPUs to CoreWeave and guarantees to buy back any unused capacity.

xAI finances billions of dollars in chips through a special-purpose vehicle that leases them back over a five-year period.

Meta and Oracle fund data centers with debt collateralized by the very GPUs they’re using.

Amazon invests in Anthropic, which in turn spends heavily with AWS.

Each deal makes sense on its own, driven by strategic alignment, access to supply, and ecosystem growth. But together they raise a more complex question: how much of this demand is organic, and how much is creative financial choreography designed to keep the growth flywheel spinning?

And there is a lot at stake. The AI race is rapidly changing the world, and the Mag 7 knows that history doesn’t favor them remaining the largest companies in the next decade if they don’t change with it.

As Zuck said in a recent interview:

“We are going to spend aggressively. Even if we lose a couple of hundred billion, it would suck, but it’s better than being behind the race for super intelligence.”

It’s also worth mentioning that it’s not just a race between companies, but also a race among nation-states. The US is the current global platform for freedom, financial markets, and the world’s reserve currency, as one founder of an AI company put it to me recently on this topic:

“We also want to be the global platform for AI compute”

On the other hand, there simply isn’t enough capital available, and at this stage in the cycle, creativity fills the gaps. And there is no one more creative and worried about the paradox above than Sam Altman and OpenAI, who seem to be announcing a new deal every week, including last week’s with AMD, which included a circular-ish option for OpenAI to purchase up to 10% of AMD, and this week’s multi-billion dollar partnership with Broadcom.

However, history reminds us that circular growth can appear to be progress until it isn’t, and capital becomes expensive again.

The Rise of the Neoclouds

Until recently, I knew very little about neoclouds – GPU-first providers renting compute to labs hungry for capacity. Their leader, CoreWeave, went public earlier this year. The term itself feels paradoxical: “GPU-first” and “cloud provider” are related, yet different.

Neoclouds are not hyperscalers. They do not sell storage, databases, or enterprise software. They purchase GPUs in bulk, wire them into dense clusters, and lease raw computing power to model builders who cannot obtain enough from Amazon, Microsoft, or Google. They exist because demand has outrun supply. According to reports, there are now approximately 190 of them. The largest, CoreWeave, earns over 60 percent of its revenue from Microsoft, a reminder that in this market, customers and competitors often share the same balance sheet.

CoreWeave’s founders came from the commodities and energy trading industries, not cloud infrastructure. That background gives the company a trader’s mindset: move fast, manage volatility, arbitrage supply. Before the IPO, they reportedly took $500 million off the table. Following the lock-up, insiders sold an additional $1 billion, and Magnetar, a major investor, sold $1.9 billion worth of shares. None of this is unusual; investors are entitled to take profits. But it does invite comparison. When Jeff Bezos watched Amazon’s stock fall from $113 to $6, he didn’t sell. He told investors that the company was getting heavier by the day and continued to build. If these insiders saw the same kind of weight forming beneath CoreWeave, would they be this eager to exit?

The economics are still forming. CoreWeave depreciates its GPUs over six years; peers like Nebius use four. Nvidia now refreshes chips annually, and Jonathan Ross of Groq argues that modeling three- to five-year GPU lives is “wrong.” At Groq, they amortize over one year, because “the economics of acceleration move that fast.”

It’s not the first time growth has outpaced accounting. In March 2000, MicroStrategy restated two years of earnings after realizing it had booked multi-year contracts as revenue for the current year. It was not fraud, just a matter of timing. But the correction erased profits, wiped out 60 percent of the company’s value in a day, and forced investors to confront how much of the era’s growth was built on assumptions. The echo today lies in how AI firms depreciate GPUs and capitalize infrastructure build out.

If Ross is right, many of these assets will age faster than they are written down, making near-term profits look stronger than the underlying economics. Still, neoclouds remain important players. They absorb capital that hyperscalers hesitate to spend, convert it into operating expense, and keep the training runs moving.

They play a vital role in the AI economy. It’s just hard to ignore how creative it’s all getting at this stage in the cycle and how familiar that creativity feels.

Why It Matters

We’re in an AI bubble, and the benefits will be gigantic. AI’s potential is extraordinary, but so is the exuberance surrounding it. The market is full of creativity. Some of it is genuine, some of it is circular. This is a paradox we must be able to hold without paralysis. The ability to hold two opposed ideas at once and still function. Both can be true. The voting machine will reward narrative for a while. The weighing machine will decide what endures. For our readers, that is the work. To see clearly, to stay sharp, and always ambitious.

Best of the rest:

💸 It’s The End of the (ARR) World and I Feel Fine — If AI software is “hired” labor, ARR and multi-year lock-ins lose signal, forcing vendors toward variable pricing, proof-driven adoption, and investor models that reward measurable outcomes over renewals. — Brett Queener

🤖 Technological Optimism and Appropriate Fear — Jack Clark warns that frontier AI is advancing faster and becoming more self-aware, urging policymakers and builders to balance optimism with transparency and real fear as systems grow beyond human understanding. — Import AI

🏛️ Stop Avoiding Politics — Engineers who reject “office politics” don’t escape it; they just forfeit influence to those who understand how decisions actually get made. Politics isn’t manipulation—it’s how good ideas survive. — Terrible Software

🔮 Prediction Is the New Postmodernism – Alex Danco argues that “prediction” isn’t just a market mechanism but the defining worldview of our era, replacing postmodernism’s self-referential rendering with a culture organized around foresight, speculation, and participation in one grand predictive game. – a16z Substack

💼 Why AI Will Widen the Gap Between Superstars and Everybody Else – New research argues that AI won’t level the playing field but instead amplify the advantages of top performers who have the expertise, autonomy, and curiosity to exploit its full potential—forcing companies to rethink how they train, evaluate, and reward talent in an AI-first workplace. – The Wall Street Journal

💰 OpenAI makes a five-year business plan to meet $1T+ spending pledges – Backed by $13B in annual recurring revenue—mostly from ChatGPT—OpenAI is pursuing new revenue streams, debt partnerships, and fundraising to finance massive compute and infrastructure costs. – Financial Times

Charts that caught my eye:

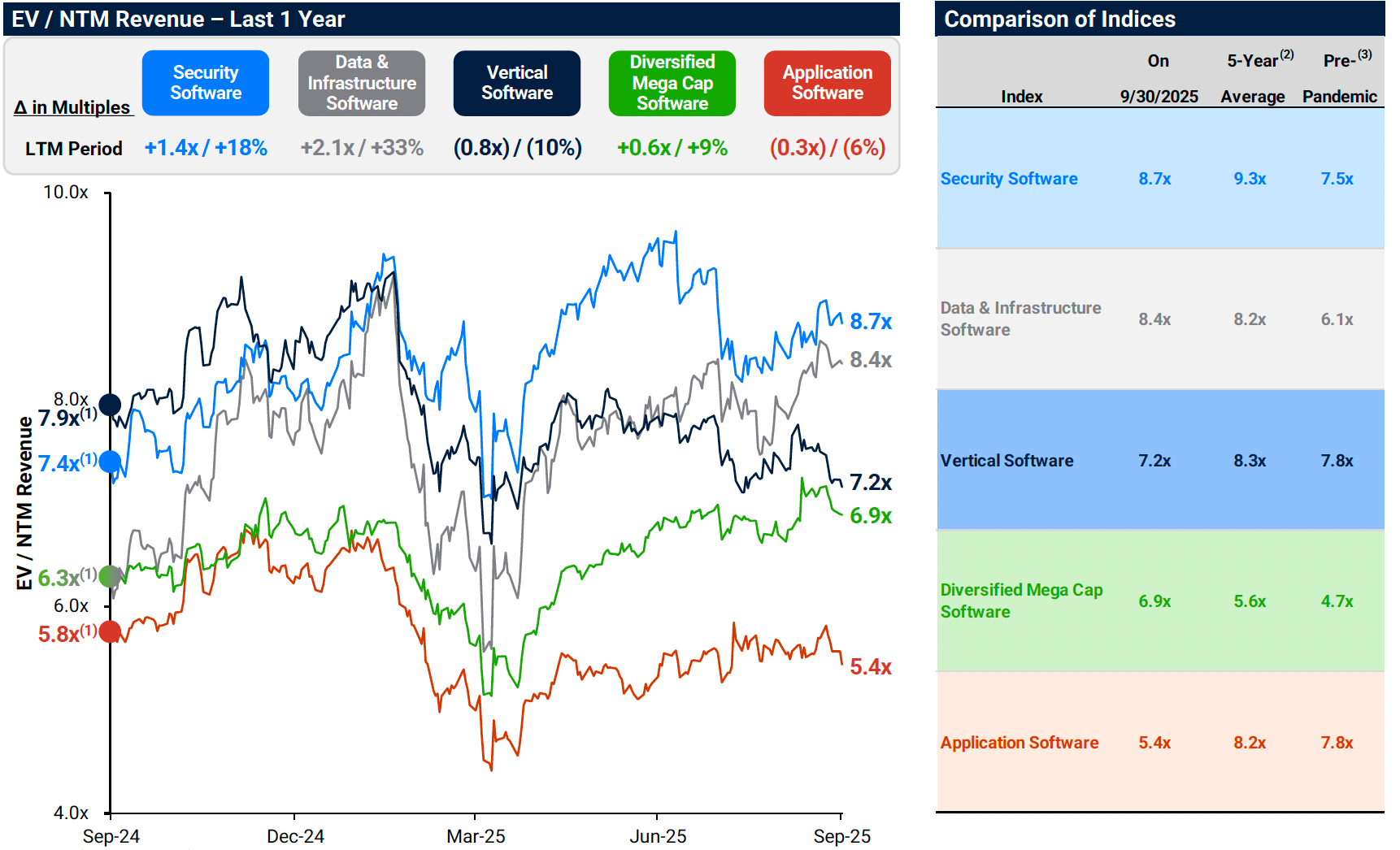

→ Why does it matter? Security software trades at a premium for a reason. The attack surface grows ever larger, and the line between “security” and “infrastructure” has blurred. What used to be insurance is now essential plumbing, and the market is repricing that reality.

→ Why does it matter? The internet, as we know it, is changing rapidly. A whopping 52% of content on the internet is now written by AI. This will only get worse as the AI trains on existing content, which means it’ll be training more and more on AI slop. We’re all developing “AI slop” filters that are going to relentlessly prioritize the sources we’re all consuming.

→ Why does it matter? JP Morgan announced this week plans to invest $1.5T over the coming decade. Here are the 4 major themes they plan to focus on.

Tweets that stopped my scroll:

→ Why does it matter? The boundary between software and the physical world is dissolving. Figure 03 marks a turning point in robotics. It’s not just a prototype that walks—it’s engineered for scale, with tactile hands, on-board AI, wireless charging, and a production line already built. The claim that “nothing in this film is teleoperated” signals a quiet milestone.

→ Why does it matter? Salesforce and OpenAI just collapsed the boundary between enterprise software and AI’s most popular product. Agentforce 360 now lives inside ChatGPT, while ChatGPT itself lives inside Slack. That means querying CRM data, generating insights, and completing transactions all flow through a single conversational layer.

→ Why does it matter? This is an incredible piece by Jeremy Stern and the team at Colossus, and it’s totally not what you’d expect. To understand Josh and Thrive, Jeremy offers a wide-ranging profile going back multiple generations, the hardship they endured, the immigrant mentality, the pursuit of the American Dream, and what has made Thrive into one of the best venture investors of the current era, the next JP Morgan, they quietly allude to in the profile. Carve out the time to give this a read.

Worth a watch or listen at 1x:

→ Why does it matter? Arthur Brooks is reframing happiness as a skill, not a circumstance. By breaking it into enjoyment, satisfaction, and meaning, he turns fulfillment into something you can train rather than chase. His journey—from economist to happiness scholar to Oprah collaborator—illustrates that purpose compounds through reinvention. In a culture that confuses success with joy, Brooks reminds us that real happiness isn’t found in outcomes but in how we live between them.

→ Why does it matter? A wide-ranging conversation with Jack Altman and Vince Hankes, Partner at Thrive Capital. What I enjoy about Vince’s stories is how hands-on Thrive gets with their investments. Vince talks about the “barbell” effect in venture capital, which is common in mature industries. VC as an asset class is entering that stage.

Quotes & eyewash:

→ Why does it matter? The merchant of infinite loop. This one had me laughing out loud.

→ Why does it matter? I’m excited to pick up Andrew Ross Sorkin’s new book, 1929! Sorkin wrote Too Big to Fail. I’m already a few chapters in, and it’s great. Pick up your copy here.

The mission:

The Wall Street Journal once used “Read Ambitiously” as a slogan, but I took it as a personal challenge. Our mission is to give you a point of view in a noisy, changing world. To unpack big ideas that sharpen your edge and show why they matter. To fit ambition-sized insight into your busy life and channel the zeitgeist into the stories and signals that fuel your next move. Above all, we aim to give you power, the kind that comes from having the words, insight, and legitimacy to lead with confidence. Together, we read to grow, keep learning, and refine our lens to spot the best opportunities. As Jamie Dimon says, “Great leaders are readers.”

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or legal advice. Readers should do their own research and consult with a qualified professional before making any decisions.